Residual Profit Partnership

Partnerships Partnerships This Is When Two Or More Persons Enter Into A Business Venture With The Intention To Make Money Partnership Agreement Legal Ppt Download

Partnership Appropriation Account Double Entry Bookkeeping

Partnership Accounts 6 2 Formation Of A Partnership Defined In The Partnership Act 1890 As The Relationship Between Two Or More People Engaging In Ppt Download

1 Accounting For Partnership Learning Outcomes Understand The Concept Of Partnership Understand The Journal Entries For The Formation Of Partnership Ppt Download

Study Tips Final Accounts Preparation Appropriation Accounts Aat Comment

The Profit Split Method With Example Transfer Pricing Asia

Residual profit - Profit available for splitting to the partners after all appropriations are done.

Residual profit partnership. The residual profit is the amount of profit remaining after taking into account the fact that the partners will be entitled to a proportion of the profit under the terms of the partnership agreement. However if there is no written or oral agreement among the partners the Law prescribes that profits and losses should be shared equally by the partners. The residual profit split method requires the identification of the routine profit for an entity as a first step.

- Remaining profit will be distributed to the partners in the profit loss sharing ratio as agreed in the Partnership Agreement. Use Of Profit Split Method In Practice. However certain adjustments such as interest on drawings capital salary commission to partners are required to be made.

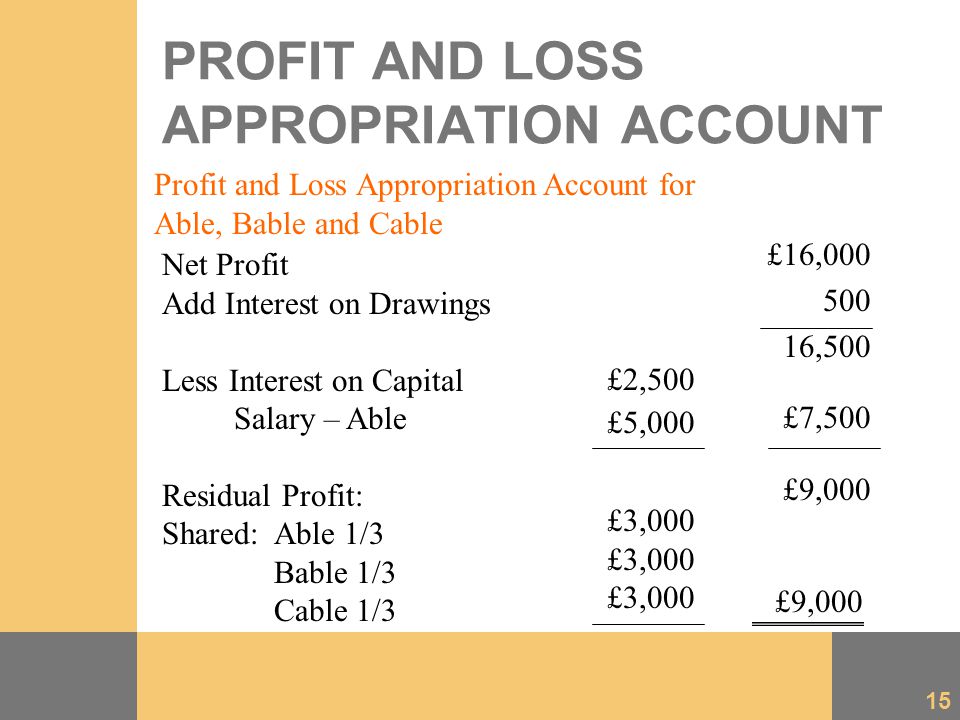

A partnership appropriation account is an intermediary account between the profit and loss account of the partnership and the individual capital accounts of each partner. The total book value of the partnership is equal to the combined value of the partners capital and current accounts or 122300 60000 12800 40000 9500 The partnership is valued at 164300. In 1920s General Motors used the concept to evaluate its business segments.

Step 1 Calculate goodwill. Profits or losses made by a firm should be divided among its partners in accordance with the provision of their Partnership Deed. The purpose of the partnership appropriation account is to allow adjustments to be made to the net income from the profit and loss account before distribution of any residual net income is made to the partner capital accounts.

The residual profit is the amount of profit remaining after taking into account the fact that the partners will be entitled to a proportion of the profit under the terms of the partnership agreement. This is not a charity but a service provider charging fees for its services which is its only source of income. For this purpose it is customary to prepare a Profit and Loss Appropriation Account of the firm.

In a partnership it is the residual profit which is divided between the partners in the profit and loss sharing ratio. The residual profit is the amount of profit remaining after taking into account the fact that the partners will be entitled to a proportion of the profit under the terms of the partnership agreement. Managerial accounting defines residual income in a corporate setting as the amount of leftover operating profit after paying all costs of capital used to generate the revenues.

Study Tips Advanced Aspects Of Appropriation Accounts And Effective Communication Aat Comment

Partnership Accounting Unit 3 Further Aspects Of Financial Accounting Mr Barryyear 13 A Level Accounting Ppt Download